The sales pitch that AR automation will replace commercial collections entirely is a persistent one, and it is wrong in a specific way. Platforms like HighRadius or Billtrust handle accounts that are still inside the normal payment relationship. These are customers who will pay given the right reminder at the right time. They are not built for customers who have already decided not to pay. Those accounts need something the software cannot provide, which is why the growth of the platform market and the need for commercial collections are not in competition.

When deciding how to handle receivables, it is important to remember that time is money. Controllers, your responsibility is managing the company's money, and every minute you spend attempting to recover a lost balance is time taken away from managing real cash flow. Credit Managers, your primary concern must be the extension of credit rather than acting as a full-time follow-up service. Automation buys back your time by pushing invoices out on schedule and keeping follow-up consistent across hundreds of open accounts so nobody has to babysit the ledger.

The pitch is easy to believe because a better process naturally reduces unpaid invoices. What the marketing leaves out is what happens when the process runs exactly as designed and the invoice still sits open. By ninety days late, the customer already knows they owe the money, meaning another automated reminder changes nothing. How much of your time are you spending looking for lost money when the software has already done its job?

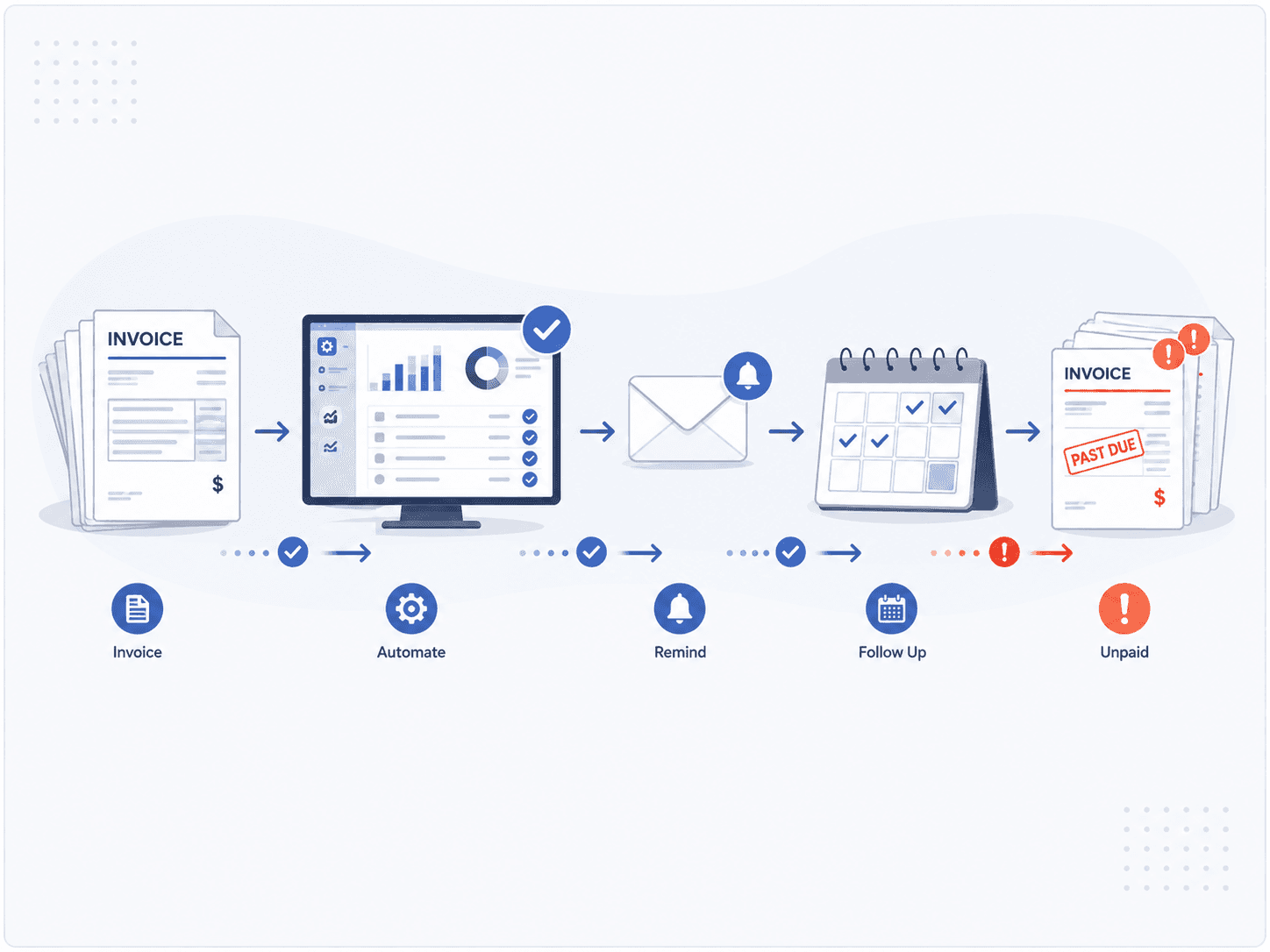

Accounts receivable solutions cover a wide span of the invoice-to-cash process. Invoicing and delivery, dunning sequences, cash application, payment portals, credit scoring, and aging analytics all live under that heading, and the larger platforms bundle most of them. Every one of those functions operates on the creditor's side of the ledger, governing when the invoice goes out and how consistently the reminder repeats after it. The customer's decision about whether to pay sits outside all of them.

| What the category covers | Where it stops |

|---|---|

| Invoicing and delivery | The invoice arrives, and whether it gets prioritized stays the customer's call |

| Dunning and reminder sequences | The message repeats on schedule after the customer has stopped reading it |

| Cash application and payment portals | There is nothing to apply until the customer decides to send funds |

| Credit scoring and risk flags | The flag comes before the sale, while an open balance needs a different tool |

| Aging and DSO reporting | The report shows the account sliding and moves no money by itself |

The limits of a perfect sequence

An AR platform makes sure the creditor holds up its own end by sending the invoice on time and delivering reminders on a schedule instead of whenever someone happens to remember. Keeping the account in a steady queue rather than letting it slip between desks provides a level of consistency that is well worth paying for when a company carries thousands of open receivables. Automation effectively shrinks the category of accounts that go unpaid simply because nobody followed up.

The software also keeps a record that shapes how much money comes back the day an account finally needs outside help. An agency that receives a clean history sees exactly when the invoice went out and how the customer answered at each stage, allowing them to begin working the balance the same day. Handing that same agency a dollar figure and a company name forces them to spend their first days rebuilding a history the creditor already lived through.

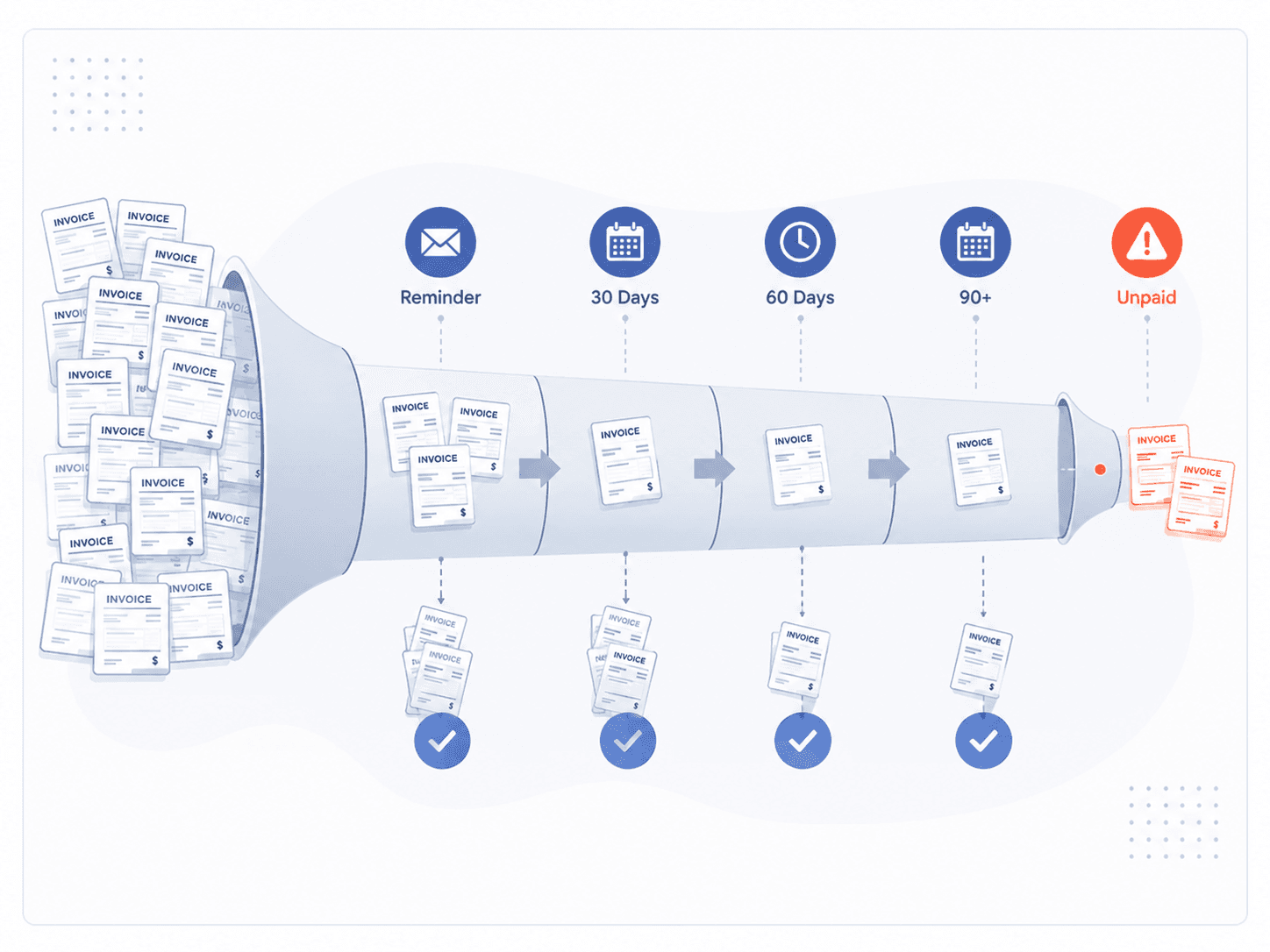

The automated sequence moves from thirty days to sixty to ninety while every message drops into an inbox the customer sorted to the bottom weeks ago. An account can travel through the entire workflow exactly the way it was built to and still close the month unpaid.

The account that survives the workflow

By ninety days past due, the customer has already received the original invoice alongside a stack of reminders. The balance stays open for entirely different reasons, whether the customer is working through a cash flow squeeze or sitting on a dispute they never raised formally but lean on to justify waiting. They might run a payables process that pays by relationship weight and keeps you beneath the vendors who press harder. Underneath all of these excuses is a simple read on their part that you have not yet made the balance uncomfortable enough to move it up the list.

Another reminder simply repeats the same message the customer has already learned to absorb. Every deadline that passes without consequence teaches the customer how seriously the balance is being taken, and a follow-up sequence with no escalation behind it repeats that lesson on a schedule. By the time the platform flags the account as high risk, the customer has had months to form a view about your willingness to act.

A team freed from manual follow-up can finally see its own receivables clearly because the balances still standing after a working automated process runs are the ones that will never answer another email. Automation pulls them out of the noise so the company recognizes what it is actually holding. The better the software gets, the more cleanly it isolates the accounts that need a phone call and real leverage behind them.

Does AR automation work better than hiring more collectors?

For the follow-up work, yes, though the reason has less to do with software than with who you can actually hire. A collector coming off consumer accounts arrives trained on call scripts and volume dialing, while commercial work asks for someone who can argue a variance in a purchase order against the contract that governs it. The crossover runs about a year, and turnover in the role means plenty of hires leave before they finish it.

The harder problem arrives after the hire works out. Look at what happens to the aging report of a company that adds a strong collector. The thirty and sixty-day buckets tighten, because steady pressure is exactly what those accounts were missing. The ninety-plus column stays about the size it was. A good internal collector calling a customer who has already decided to hold the balance is still a vendor calling about an invoice, delivered by someone more expensive than the software.

Cost structure settles the rest. A salary is owed every month regardless of what comes back, and so is the subscription. Contingency only costs money on balances that resolve. There is a volume problem underneath it too, since a commercial collector working properly carries a couple hundred active files, and a company placing a dozen accounts a quarter has hired someone who will spend most of the year underused.

The weight of a third party

Bringing in a collection agency changes the status of the account because the customer is no longer managing a routine payable from a vendor who keeps emailing. The balance moves out of the original business relationship and into formal recovery, carrying a weight no scheduled message from you will ever match.

A commercial agency working a B2B account reads the contract and tells a genuine dispute from a stall dressed up to look like one. The handoff itself sends a message that the account has left the pile the customer was free to keep deprioritizing, meaning that clearing it now takes more than letting one more reminder go unanswered.

Companies put this moment off because escalation feels like admitting the relationship has failed, and nobody wants to be the one who makes that call. The relationship already changed the day the customer stopped paying, and placing the account simply answers that change. Waiting longer gives the balance more room to age while giving the customer one more stretch of evidence that nothing is going to happen.

The file that arrives with the account

This is exactly where automation benefits collections the most. Automation makes the hard accounts easier to work once they arrive because a file that shows up with its full history attached is one an agency acts on the same day. Conversely, a file that shows up as a balance and a name forces the agency to spend its first and most valuable days rebuilding what already happened.

That history changes how the account gets handled. A customer who disputed the balance in March and then ignored the resolution offer calls for different handling than one who ignored every notice from the first invoice forward. A customer who paid half in February and then stopped tells a different story than one who denied owing anything at all. Automation keeps those distinctions on the record so they do not live in one person's inbox or walk out the door when the account manager takes another job.

When the record is clean, the agency skips the discovery phase and goes straight to working the balance. The longer a balance sits, the harder it becomes to collect, meaning every week spent rebuilding a history comes directly out of what the company stood to recover.

Automation will keep getting better and more companies will adopt it, which only makes the list of stubborn accounts easier to see. The companies that get the most out of it know where its job ends, keeping the record clean and reading what is still standing at the end for what it is. Our warning signs checklist covers the signals worth catching before an account reaches that point, and the placement form is the faster route for the ones already there. The software and the agency handle two distinct halves of getting paid.

Frequently asked questions

- Does AR automation work better than hiring more collectors?

- For follow-up work, yes. A platform sends reminders on the same schedule every time, while a person doing that job misses accounts during a busy close. The comparison gets harder on accounts that need judgment, where a collector reads the contract and hears whether a controller is stalling. That skill takes a year or more to develop in a new hire. Cost structure usually settles it. Software and salary are both fixed costs owed whether the account resolves or not, while contingency moves with the outcome, costing nothing until money comes back.

- Does AR automation replace the need for a collection agency?

- AR automation improves the creditor's own process by sending reminders and keeping follow-up documented. A collection agency becomes relevant once that process runs its course and the customer still has not paid, proving the two tools do different jobs and the growth of one does not remove the need for the other.

- When should an account move from AR automation to a collection agency?

- An account should move when internal follow-up stops producing movement. Common triggers include an account past 90 days with no payment or repeated broken promises, as well as a customer who stops responding or a dispute that stays open despite multiple attempts to resolve it.

- How does AR documentation help a collection agency?

- A collection agency that receives a well-documented account starts from a position of knowledge rather than guesswork because it sees the exact timeline of invoices and reminders. Tracking who was contacted and how they responded to disputes or partial payments changes how the agency reads the account and approaches the customer.

- What do accounts receivable solutions handle?

- Accounts receivable solutions handle the creditor's side of getting paid, which includes issuing and delivering invoices, running reminder sequences on a schedule, applying incoming payments, scoring credit risk, and reporting on aging. The category assumes a customer who will pay once the process runs correctly. Accounts where the customer has reviewed the balance and chosen to hold it fall outside what these platforms are built to resolve.

- What is the difference between dunning and collections?

- Dunning is internal follow-up from the original creditor sent through the same relationship and the same company that issued the invoice. Collections brings in a third party to change the status of the account so the customer is no longer managing a routine payable. The balance moves into formal recovery, carrying a weight an automated reminder lacks.

Read next

When to Stop Sending AR Reminders and Escalate to CollectionsThe 30/60/90-day handoff question: at what point does sending another reminder stop being the right move? Here is a practical framework for the accounts your automation left unresolved.Have an account ready to place?

We work on contingency. No upfront cost.

JSD has been handling commercial collections since 1997. Our team reviews every account directly. No intake queue, no automated triage. Most clients are up and running the same day.