Search for how to pick a collections agency and you will find the same article written about forty different ways, nine-step guides and vetting checklists that tell you to check the license, ask about the fee structure, look them up with the Better Business Bureau. The advice is reasonable, and almost none of it touches the decision that actually matters. If you want to understand why a third-party agency carries the weight it does before getting into how to pick one, this piece on the stigma around collections is worth reading first.

The short version, for anyone who needs it before reading further: when another business owes you on an unpaid invoice, the right partner is a commercial collections agency rather than a consumer debt collector. Look for genuine B2B experience, contingency fees that cost nothing unless they recover, verifiable licensing in your debtor's state, disciplined documentation practices, and a communication style you would trust with your own customer relationship. The rest of this article explains why each of those matters more than the usual checklist suggests. For a structured version of that evaluation, including prompts you can hand to an AI tool while you research, see our guide on how to choose a commercial collection agency.

The checklist frame treats picking a collections agency like buying a piece of software, something you evaluate on features, price, and credentials before moving on. Picking the agency that will represent your company to a customer you already lost money on is a different kind of decision, and the checklist frame was not built for it.

The question worth asking first

Before you start evaluating agencies, it is worth being honest about what is actually sitting on your desk. You extended credit to another business. They received what they ordered. The invoice has aged past the point where your own follow-up was moving it. What you have now is a balance a customer received the goods for and still owes, and the next step is a third party asking for it on your behalf.

The agency you hire will be the next voice that company hears on this invoice. How that voice comes across reflects directly on you. Your customer experiences the agency as an extension of how you chose to handle the dispute, and a call that comes across as aggressive or transactional lands as your decision, not the agency's.

The reputation question matters for that reason, and most checklists treat it too superficially. A polished website and a few trade badges say nothing about whether an agency can speak to a controller without scorching the relationship. The better question is simpler and harder to answer from a website. Would you trust this agency to speak for your company to a customer you might still want to do business with?

Why the type of agency matters more than it seems

Commercial collections and consumer collections look like the same business from the outside, and the difference runs deeper than most people expect. Consumer collections is governed by the Fair Debt Collection Practices Act, which sets detailed rules around contact frequency, language, and dispute handling, all of it written to protect individuals from aggressive recovery tactics. A consumer shop's entire operation, from its scripts to its compliance software, is built around high volume and that rulebook.

B2B commercial debt generally sits outside the FDCPA's consumer-debt framework, though state laws, contract terms, and the general prohibitions on unfair or deceptive practices still apply. But the legal difference is honestly the smaller part of it. What really separates the two is the nature of the problem itself.

A past-due invoice from a business customer is usually a purchase order dispute, a backlog in accounts payable, a cash flow problem, a change in personnel, or a company that has quietly decided which vendors can wait a little longer. The work rewards someone who can read a contract, find the right person to talk to, and tell a genuine dispute from a stall. A consumer agency's workflow was built for high-volume individual accounts, and those skills transfer poorly.

You are unlikely to hand a business account to a pure consumer agency by accident, because they would probably not take it. The real risk is the generalist who accepts both kinds of work and has built depth in neither, or the high-volume shop rooted in consumer collections that runs your commercial account on consumer instincts. The file moves through a system that was designed for a different kind of problem. When you have past-due B2B invoices that need commercial collection services, you want an agency that works B2B accounts the way the work actually functions.

Timing is where most businesses leave money on the table

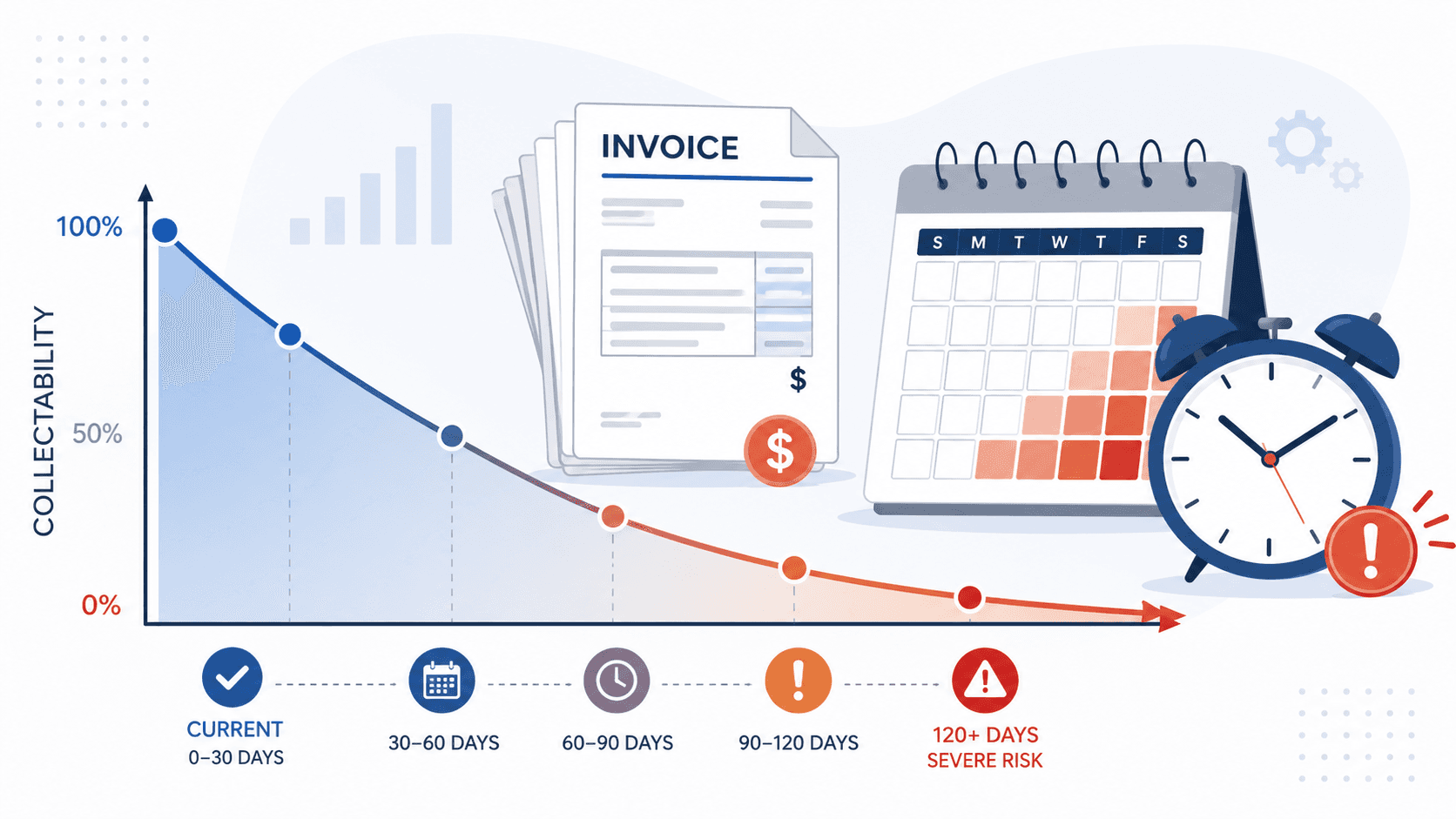

There is one finding in commercial debt recovery research that never really changes: accounts get harder to collect the longer they sit. The Commercial Law League of America has tracked the pattern for decades. An account is collectible around 94% of the time at 30 days past due. By 90 days that number is down to 74%. At six months it is 58%. At a year it is 27%. The curve bends hardest in the first 90 days, which is exactly where most businesses wait the longest.

They wait because escalating feels awkward, because they do not want to upset the customer, because someone in accounting is still following up even though the follow-up stopped producing results weeks ago. Every month of silence teaches the debtor that ignoring the invoice carries no real consequence, and each month that lesson gets a little more comfortable.

By the time a business finally places an account at 120 or 150 days, the agency is recovering a debt and undoing months of weak signaling at the same time, and the second task makes the first one harder. If you are reading this with an account already past 90 days, place it now rather than waiting for a cleaner moment. If you are reading this before that point, the most useful thing to take away is a lower threshold for escalating than you probably have right now.

What actually separates one agency from another

Licensing matters and you should verify it. Reputable agencies are licensed, bonded, and members of trade organizations like the Commercial Law League of America or the Commercial Collection Agency Association. Every serious agency already has those credentials, so they tell you who clears the bar and almost nothing about who clears it best. What actually separates one agency from another tends to be harder to find on a website.

Industry familiarity is one real differentiator. A past-due account in manufacturing involves different documentation, different dispute patterns, and different relationship stakes than one in staffing, logistics, equipment leasing, or professional services. An agency that has worked your sector for years has already seen the disputes that come up, knows which ones resolve quickly and which ones need a different approach, and arrives already knowing the terrain your accounts sit in.

The other thing worth asking directly is how they handle the customers you might still want back. A customer who paid reliably for three years before running into a bad quarter is a different conversation than one who was always slow to pay. An agency that treats those two the same way is using your file as a transaction, and the relationship damage tends to follow.

Questions to ask before hiring a collections agency

A short call answers more than a website ever will. Find out what percentage of their current placements are commercial B2B accounts rather than consumer debt, how they handle a disputed invoice when the debtor claims the goods or pricing were not what was agreed, and what documentation they need before they can place an account. Ask how they would describe their tone with debtors, when they recommend litigation, and what you owe if they recover nothing.

The agency that answers the documentation and dispute questions with specifics has actually done this work many times. The one that goes vague, or treats litigation as a straightforward yes-or-no, is also telling you something. A confident answer that starts with "it depends, and here is what it depends on" is almost always the better sign.

What working with an agency actually looks like

Placement is straightforward when the file is clean. You hand over the invoice, the underlying contract or purchase order, and whatever record exists of your own collection attempts. The agency reviews the file, verifies the debt is valid and within the statute of limitations, then sends a formal written demand and begins direct contact with the debtor.

The goal from the start is to find whoever actually has authority to release payment. In commercial collections, reaching a receptionist is a different outcome from reaching a controller, and reaching a controller is a different outcome from reaching the owner, and the file moves differently depending on which conversation happens first.

For a meaningful share of accounts, the agency's involvement alone is enough to break the logjam. A creditor's own team calling reads as routine follow-up. A third-party commercial collection agency calling signals that something has changed, and debtors tend to notice that signal even before anyone has said anything consequential. Where the debt remains unpaid, the agency can report the balance to commercial credit bureaus, which adds another layer of consequence for a debtor who had been comfortable ignoring the original creditor. Most accounts resolve through negotiation, whether that means payment in full or a structured plan. Litigation is a last resort, and a good agency tells you honestly whether an account is worth that path before you commit to the cost of it. Learn more about our commercial collection process for unpaid business invoices.

The frame that actually helps

Verifying the license, understanding the fee structure, asking about industry experience, every item on the standard checklist is genuinely worth doing.

The checklist is the starting point, and the real decision sits past it. The real question is who you want speaking for your company once the relationship has already broken down. An agency can satisfy every item on the checklist and still be the wrong answer to that question, and that gap lives somewhere a website can rarely show you.

JSD has recovered unpaid invoices from business customers for other businesses since 1997, on commercial accounts across the United States. If you have a past-due account from a business customer, you can place it in one business day with no fee unless we recover. Send us the account and we will tell you honestly whether it is worth pursuing before you commit to anything.

Frequently asked questions

- When should I hire a collections agency for unpaid invoices?

- The general rule is 60 to 90 days past due, once your own follow-up has stopped producing results. Recovery rates drop sharply after 90 days. Commercial Law League of America data shows an account is collectible around 94% of the time at 30 days past due, 74% at 90 days, 58% at six months, and just 27% at a year. Every extra month tells the debtor that waiting carries no real cost.

- Does a collections agency need to specialize in B2B accounts?

- Yes, and the difference matters more than most business owners expect. Consumer collection agencies operate under the Fair Debt Collection Practices Act and are built around high-volume individual accounts. A commercial collection agency works under different legal rules, with different norms around communication and negotiation, and with experience in trade credit disputes, purchase order issues, and the relationship dynamics specific to business-to-business accounts. The tactics are not interchangeable.

- What does a commercial collection agency charge?

- Reputable agencies often work on contingency, meaning no fee unless they recover something. Rates typically depend on the age of the account, the balance size, the debtor's location, and how much documentation you can provide. Older accounts and smaller balances usually carry higher rates because they are harder to collect. Before placing an account, ask what the fee is, when it applies, and whether anything is owed if the account goes uncollected.

- Will hiring a collections agency damage my relationship with the customer?

- It depends on how the agency handles the account. A professional commercial agency treats the debtor as a business and works through documentation, negotiation, and direct communication. Many creditors recover the balance and continue doing business with the debtor afterward. The risk of relationship damage is real, but it tracks the quality of the agency far more than the decision to use one.

- Can a collections agency collect from businesses in other states?

- Yes, but the agency needs to follow the rules that apply where collection activity occurs. Many states require licensing for collection activity within their borders, and an unlicensed agency can create problems for the creditor. Before placing an account, ask whether the agency is licensed or otherwise authorized to handle accounts in your debtor's state.

Read next

The Commercial Debt Recovery Process ExplainedHow commercial debt recovery actually works, from the first missed payment through agency placement, negotiation, and legal escalation. What every creditor should know before the sixty-day mark.Have an account ready to place?

We work on contingency. No upfront cost.

JSD has been handling commercial collections since 1997. Our team reviews every account directly. No intake queue, no automated triage. Most clients are up and running the same day.